Dave Ramsey has a lot to say about ideal household budget percentage guidelines. And it’s hard to argue with the success he’s had in inspiring millions to get out of debt and live within their means. The Dave Ramsey budget percentages are a great tool to get your household budget on track.

One of the first steps to budgeting is actually making a budget.

Obvious? Yes. But it’s also where a lot of people seem to get stuck.

That’s why I found Dave Ramsey’s budget percentage guidelines so helpful when I first started tracking my spending. And while everyone’s situation is different, I think they are a good place to start.

Pssst… Make sure you scroll all the way down to get your own free printable copy of Dave Ramsey’s budget percentages (don’t worry, no opt-in required).

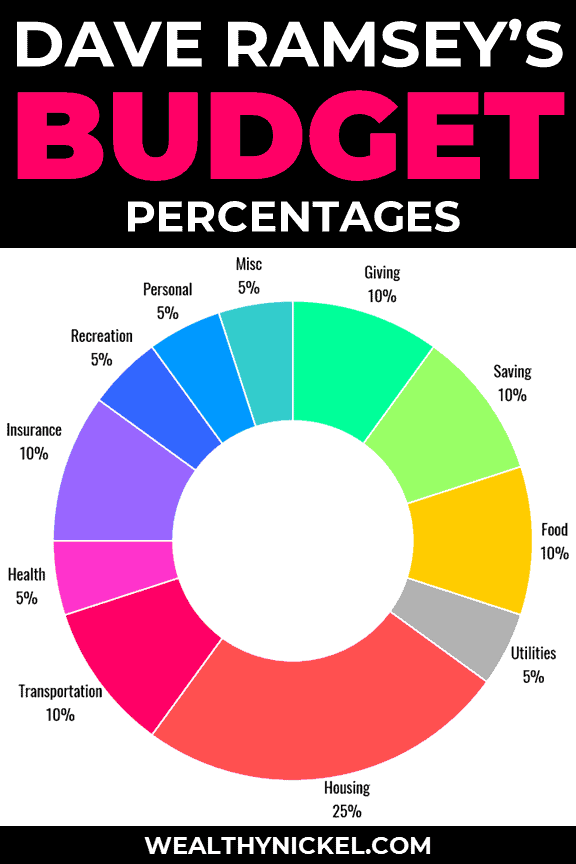

Dave Ramsey Budget Percentages

If you don’t know where to start with budgeting, here are Dave Ramsey’s recommended household budget percentages and categories that he recommends starting with. These budget percentages are based on your total after-tax income, but before you take out things like health insurance or 401(k) contributions from your paycheck.

- Giving – 10%

- Saving – 10%

- Food – 10 to 15%

- Utilities – 5 to 10%

- Housing – 25%

- Transportation – 10%

- Health – 5 to 10%

- Insurance – 10 to 25%

- Recreation – 5 to 10%

- Personal Spending – 5 to 10%

- Miscellaneous – 5 to 10%

Here is a simple budget percentage pie chart you can use as a guideline for your ideal household budget (Pin it here):

Recommended Household Budget Category Descriptions

Here’s a little more detailed breakdown with what goes in each category according to Dave Ramsey:

Giving (10%)

The cornerstone of Dave Ramsey’s approach to budgeting starts with giving to your church or other charitable causes you care about. I 100% agree on this point, and I believe giving is a big part of changing your mindset about money.

Saving (10%)

Money set aside for the future, whether building up your emergency fund or saving for retirement in a 401(k) or IRA.

Food (10-15%)

Dave Ramsey’s food budget recommendations include groceries and eating out. This can be one of the hardest categories to for people to budget for, and I know personally we have to keep an eye on it every month so that it doesn’t get out of control. If you don’t plan ahead, it can be easy to spend a lot of money on convenience foods or grabbing take out on the way home from work.

If you need some help, here are 7 ways we save money on groceries without sacrificing quality, and here is a detailed breakdown of how much you should spend on groceries.

Utilities (5-10%)

This includes electricity, water, natural gas, and trash service. While not specifically mentioned by Dave Ramsey, I would put your cell phone here too.

Housing (25%)

Your rent or mortgage (including property taxes and insurance). This is a big chunk of your budget, and a great place to try to find some savings by living a little cheaper. If you can cut your rent from $1200 to $1000 per month, that’s extra savings of almost $2500 per year – enough to fund a nice vacation! Just remember that owning a home comes with hidden costs you have to remember to budget for.

Transportation (10%)

Anything you need to spend money on to get to work, the store, or your other weekly activities. If you’re lucky enough to live in a big city and not need a car, this could be subway tickets or Uber rides. If you’re like most of us, this money goes toward your car payment, gas, and insurance.

Health (5-10%)

While you can’t really plan for health expenses, it’s good to account for them in your budget. It could be routine doctor visits, or multiple trips to the urgent care clinic over Christmas when you are sick and away from home (that was a rough holiday for our family…) At the end of the day, your health is more important than money. Make sure you’re taking care of yourself and your family.

Insurance (10-25%)

Health insurance just keeps getting more and more expensive. But you also need to consider life insurance, disability insurance, etc. in this category.

Recreation (5-10%)

Anything you do for fun. For us that would be stuff like Netflix, our gym membership (1.5 hours of free childcare a day might make this our best purchase ever!), and activities for the kids.

Personal Spending (5-10%)

Clothing, haircuts, home decor, and all that stuff you buy at Target when you spend $200 and have no idea what you bought (no, just me?)

Miscellaneous (5-10%)

The slush fund for all the stuff you forgot to budget for. Trust me, there’s always stuff you forget.

Are the Dave Ramsey Budget Percentages Realistic?

Even Dave Ramsey, famous for making rules of thumb into hard and fast edicts, says that these budget percentages are just a guideline to get started. You may have to adjust certain categories up or down to fit your particular situation.

Curious about what the average American spends vs. Dave Ramsey’s budget percentages? Check out these budgeting and spending statistics for more info. (Hint: most people tend to overspend on two main categories.)

What About Debt Payments?

The suggested budget assumes you are not carrying any debt (besides your mortgage), so if you have student loans, credit card debt, or some other form of monthly debt payments you will need to make sure you account for those in your budget.

The ultimate goal is to be spending less than you earn, so it may make sense to cut way back in some other discretionary categories for a short time until your debt is paid off.

What Percentage of Your Income Should You Save?

Dave Ramsey recommends allocating 10 percent of your budget to savings. If you’ve been living paycheck to paycheck and never had a budget before, I think this is a good place to start.

But if you are truly looking to get on the path to financial freedom, and not have to work until you’re 65 or beyond, one of the most important things you can to do to speed up the process is to increase your savings rate to 15%, 20%, or even more.

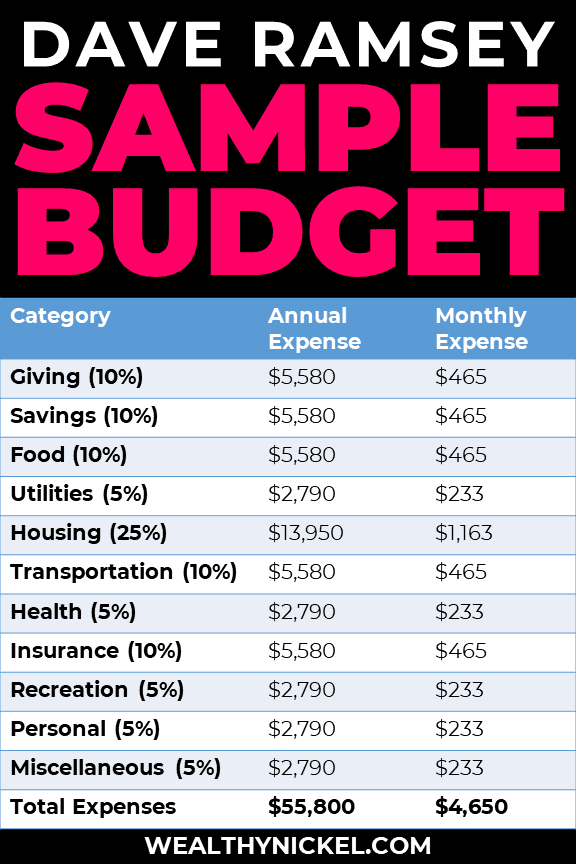

Dave Ramsey Sample Budget

So what would a sample budget look like using Dave Ramsey’s budget percentages?

Of course every family’s situation is different, but let’s take the median household income of approximately $62,000 (source). [Fun fact: the median household size is 2.5 people, so make sure to budget for your 1/2 kid!]

First, let’s assume that 10% of total income goes to taxes (a rough approximation), so that leaves $55,800 for expenses and savings in our sample budget.

By following Ramsey’s household budget percentages, here is what the median household’s budget may look like:

To me, it doesn’t look too far off, except that it might be tough to find housing for under $1,200 per month. But again, the percentages are a guideline and your budget template may look different. In the next section, I’ll take a look at my own family’s budget and compare.

How Does My Family Household Budget Compare to Dave Ramsey’s?

To give you an example of the flexibility of Dave Ramsey’s budget percentages, I thought it would be a fun exercise to compare our own household budget to his guidelines as a percentage of our income.

I know our family spends a little more in some areas, and less in others, and some things (like child care) don’t really factor into his guidelines at all. So let’s see how the Wealthy Nickel family of 4 is doing compared to the Dave Ramsey household budget percentage guidelines.

A little to my surprise, we fall into the Dave Ramsey budget plan pretty well. We are a single income family (plus side hustles), but we try to live off of just the steady paycheck. I based our after-tax income and expenses on the W-2 income and excluded all of our side hustle income.

While most of our spending falls with the guidelines, there were a few outliers:

- Giving – We gave just slightly more than 10% of our after-tax income, which makes sense because we usually aim to give 10% of gross (before-tax) income each year.

- Savings – I mentioned before that your savings rate is your biggest leverage in getting to financial independence sooner than traditional retirement age. We want this number to be as high as possible! If you include our side hustle income that all goes straight to savings, it’s even higher than 23%.

- Housing – Housing is usually a household’s largest expense. We try to live below our means here and put that money toward savings or other budget categories we value spending on. Instead of buying a 2500 square foot McMansion in the suburbs, we live in a (somewhat) modest 1400 square foot house closer to the city. We still have plenty of space for 2 small kids and don’t feel like we are sacrificing, but are saving money compared to the alternative.

- Transportation – While we have the funds currently sitting in the bank to pay off our cars, we are still carrying 2 vehicle loans. The interest rate is just too enticing to pass up and allows us to use the cash for investments, such as our real estate rental properties.

- Insurance – Honestly, I’m not sure why the recommended budget percentage for insurance is so high. Perhaps it’s to include those poor souls who are self employed and have to pay an arm and a leg for decent health insurance. I am lucky my employer provides good insurance and our contribution is relatively small. This also includes disability insurance, and separate life insurance policies for my wife and I.

- Recreation – With a 5 year old and a 3 year old, we live a pretty simple existence these days. We don’t take a lot of trips, and when we do we use credit card rewards points to pay for almost everything. As the kids get older, I expect these expenses to increase for their activities, but right now this covers Netflix, a gym membership, and the occasional movie or event.

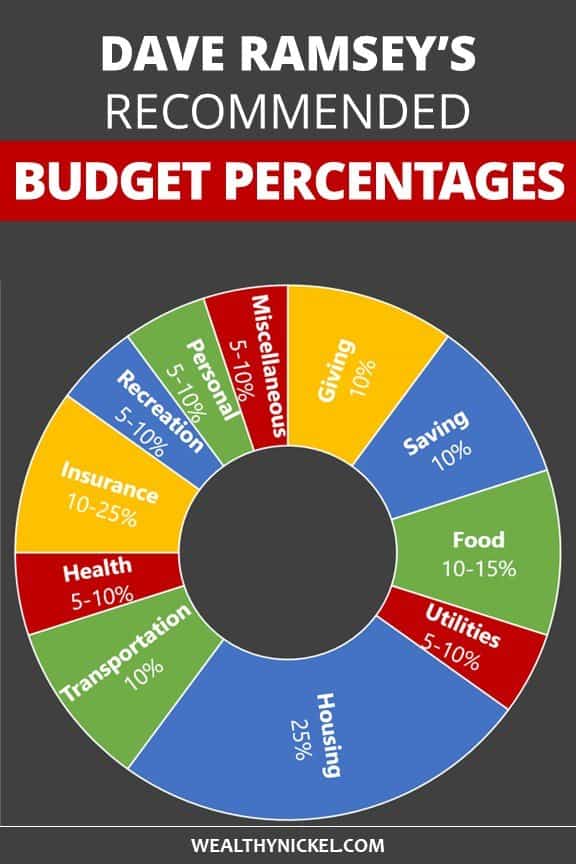

If you are more visual, here’s a helpful pie chart graphic of Dave Ramsey’s recommended budget percentages for an ideal household budget (you can also save it to Pinterest).

Other Budgeting Systems

There are a million different ways to budget, and everyone will advocate a different method. I think Dave Ramsey’s budgeting method is fairly easy to use as a starting point to craft your own budget template.

However, there are some other useful budgeting methods that may work better for you:

- 50-20-30 Budget

- Reverse Budgeting

- Paycheck-to-Paycheck Budget

The 50-20-30 Budget

Another percentage based budgeting system similar to the Dave Ramsey budget percentages, the 50/20/30 budget is a simplified budgeting method to give you a quick start guide to budgeting. In this budget, 50% of your money goes toward needs, 30% toward wants, and 20% toward savings and debt payments. Correlating them to the budget categories above, you come up with:

- 50% Needs – Housing, Utilities, Food (Groceries), Transportation, Insurance

- 30% Wants – Food (Dining Out), Recreation, Personal, Miscellaneous

- 20% Savings – Savings, debt payment

One caveat with the 50/20/30 budget method is that just because something is classified as a need doesn’t mean you can’t scrutinized that expense to save some money. For example, while transportation is a need (perhaps you need a car to get to work) – a used Toyota will get you to work just as well as a brand new Mercedes.

Reverse Budgeting

Reverse budgeting turns the budgeting process on its head, and you “pay yourself first” through savings or debt payoff.

Instead of allocating your expenses by budget category based on your available income, you first decide your savings or debt payoff goal and set that money aside before budgeting your expenses.

For example, if your goal is to payoff credit card debt, you might choose to allocate $500 per month to that goal. Make sure you schedule those payments first, and then budget your other monthly expenses afterward.

Paycheck to Paycheck Budget

The paycheck to paycheck budget is a much more intensive budgeting system, and may be more suitable if you are struggling to make ends meet.

This budgeting method gives you a deep-dive into your finances and lets you plan your income and expenses by each paycheck rather than by month. This requires more tracking and oversight, but also gives you a much better sense of your cashflow.

For more information, here is the complete guide to the paycheck to paycheck budget.

The First Step to Making a Budget That Works

If you’ve made it this far and you’re still confused as to where you should start, the #1 best thing you can do to get your finances in order is to track your spending.

There are a dozen different online tools you can use, or you can go old school and use pencil and paper. Regardless of how you do it, I can almost guarantee that tracking your spending alone will save you hundreds of dollars per month!

There is something powerful about tracking your spending. Just knowing you are doing it makes you think about every purchase, and you’ll be surprised where your money was going before you started thinking about it.

Then, by comparing your spending to the recommended budget percentages, you can see where you stack up and where you might have some room for improvement.

If you want to automate your tracking, two of the most popular tools are Mint and Personal Capital. Both allow you to import bank transactions and categorize them, making expense tracking a breeze.

The Ideal Household Budget is a Myth

While I wish I could tell you there was one ideal household budget, everyone is coming from a different background and has a different situation.

The Dave Ramsey budget percentages can be a good starting place as you begin to evaluate your spending and create your budget, but not everyone will fit neatly into the box. Personal finance is just that, personal, and a lot of factors go into how much you spend on any given category.

For example, if you live in New York City or San Francisco, your housing budget will potentially far exceed the 25% recommendation. Or if you make $100,000 per year for a family of four, it will be a lot easier to fit your food budget into 10% of your income than if you make $50,000.

There are always trade-offs to be made, but the ultimate goal remains the same. In order to achieve financial freedom, you must find a way to consistently spend less than your earn.

[ad_2]

Source link